On Digital Cash: historiography and ontology of money

Indulgences about Ideas Invent Technology, Web3 is a Deleuzian Control Society, and Value as Data

Ideas invent technology, Web3 is a Deleuzian control society, value as data

Finn Brunton

Finn Brunton

This book review also appears on Reboot's newsletter issue:

Digital Cash: The Unknown History of the Anarchists, Utopians, and Technologists Who Created Cryptocurrency is an impressive genealogy of people, ideas, and actions that lead up to the creation of digital cash and subsequently Bitcoin.

The author, Finn Brunton, primarily engages two questions:

-

How should historical narratives of culture and technology inform our understanding of the future?

-

What is the ontology of money — what makes money valuable?

While Brunton offers a ‘whirlwind tour’ of history and pokes striking questions on the ontology of money, he is rather reticent about his positions on the two questions above. However, he did remind us that Bitcoin is not inevitable nor is it sufficiently digital cash despite its ‘new kind of artificial scarcity’.

This book review also indulges into the discussion of Balaji's technological determinism, Brave browser, Dee Hock & Visa, Deleuze, Web3's claim to decentralize, and energy as currency.

Historical Narrative: Culture and Technology of Digital Cash

Brunton’s effort in crafting a historical narrative is unrivaled. Indeed, as he promises at the start, Digital Cash is ‘a whirlwind tour of many different systems of utopian desire, future fantasy, and experimental life’. He constructs two types of historical narratives: one on technology, the other on culture.

First, culturally, Brunton connects the dots and traces the futurist groups who create, coordinate, and adopt early attempts at digital cash, a recurring goal for nearly a century. He traces the history of culture and technology in parallel to arrive at his main argument that the challenge of digital cash is a challenge to ‘make digital data valuable’. In the 1930s, the Technocracy movement called for ‘autocratic master engineers’, modeling after the USSR's rapid industrialization in the early 1930s. They used energy certificates as currency, as they are ‘realer than dollars, partaking of their ontological connection to work or heat, rooted in the universe'[1]. In the 1980s, the cypherpunk movement started the American Information Exchange and the Xanadu project, aiming to make digital data valuable in itself. They dabbled in black markets for either information trading or illegal goods. Meanwhile, the Hayekian Extropians in the 1980s committed to ‘examine the alternatives of polycentric/privately-produced law and competing digital private currencies’. They dabble in cryonics as they see both digital cash and cryonics are extreme investment vehicles in the future. Digital cash would reap massive returns as it eventually renders the traditional financial system obsolete. Cryonics would restore mortality as future generations revive frozen bodies.

Brunton intended to reduce the challenge of digital cash as a part of the challenge of ‘making digital data valuable’. Is digital cash in essence about making digital data valuable? My epistemic status is low on this matter. Consider an alternative question: has digital cash historically made digital data valuable? Empirically, not always.

Instead, digital cash defines value as data. This might sound like a Wittgensteinian ‘byproduct of misunderstanding’. Yet, the subject-object distinction is important here. Digital cash defines value as data in itself. What is the value of Bitcoin? It is the numerical data of the total supply of Bitcoin (fixed) divided over the demand of Bitcoin. On the other hand, Brunton claims that digital cash makes digital data valuable. Even though in the case of Bitcoin, Brunton is correct as Bitcoin makes the digital data of ownership on a ledger valuable. A more charitable example points to attempts to link personal data to monetary rewards. Users of Brave, a web browser, can view ads while retaining personal data. In return, they are rewarded with the Brave native cryptocurrency, BAT. Brave has crossed an important milestone recently with 50 million monthly active users, unfortunately still far way from Chrome’s 3.2 billion user count. However, digital cash cannot make all types of digital data valuable. Consider the millions of lines of code that power open-source softwares are not directly economically valuable. They are used for free! The subject-object distinction, in effect, is a quantifer distinction between $\exists$ and $\forall$.

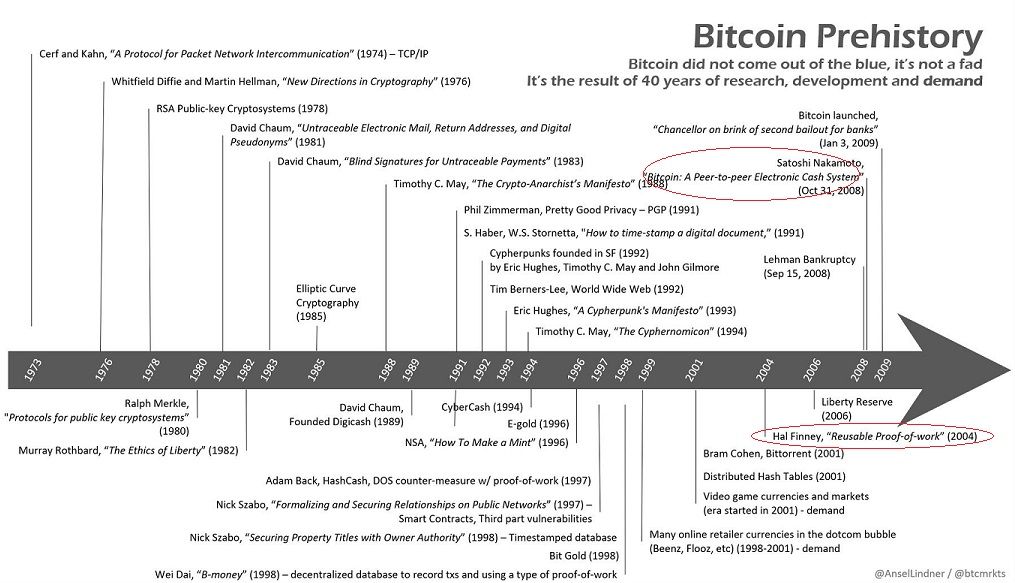

Second, technologically, Bitcoin is the culmination of technologies that stack on top of each other. Brunton starts with the Counterfeit Detection System that enforces the security of paper notes. In the 80s, digital signatures — the invention of a private-public key pair that authenticates -- was invented. In the 90s, cryptographer David Chaum launched DigiCash. It helped banks digitally issue and redeem currencies while offering anonymity to users. Even after its failure, the design framework inspired many other digital cash projects. Shortly afterward, hashing was invented. It now becomes a commonly used data structure and a cryptographic method in cryptocurrencies. These hardware and software innovations build-up to the monumental invention of Bitcoin. As Brunton writes, ‘Bitcoin wasn’t magic but a technology in context and part of that context was the power grid, the business of microchip fabrication, and the planet’s atmosphere.’

‘Bitcoin did not come out of the blue’ -- from [Bitcoin forum](https://bitcointalk.org/index.php?topic=5126554.0)

Brunton proposes that the history of digital cash shows us how money and technologies can be used to tell stories about the future — an analysis of narratives. Sadly, he does not offer any elaborations. My takeaway is that cultural movements on the fringes drive technological change in the mainstream. Andreesen Horowitz calls it Product-Zeitgeist Fit I call it that the Ideal is supreme to the Material. A reasonable reading from Brunton’s historical narrative is that technology is invented because there is a need. And this need derives from ideology and culture. In other words, Bitcoin is not inevitable. Bitcoin is circumstantial.

On another note, I was delighted to find a reference by Brunton to Dee Hock, founder of Visa. His intellectual and professional connection to crypto is much overlooked. Early in the days of Visa, before it changed hands from Bank of America to Visa’s consortium of banks, Hock envisioned payment powered by ‘Electronic Value Exchange’, free from payment rails that operate at the mercy and oligopoly of banks.

As he wrote in his autobiography:

Money would become nothing but alphanumeric data in the form of arranged energy impulses. It would move around the world at the speed of light at minuscule cost by infinitely diverse paths throughout the entire electromagnetic spectrum. Any institution that could move, manipulate, and guarantee alphanumeric data in the form of arranged energy in a manner that individuals customarily used and relied upon as a measure of equivalent value and medium of exchange was a bank. It went even beyond that. Inherent in all this might be the genesis of a new form of global currency.

If electronic technology continued to advance, and that seemed certain, two-hundred year old banking oligopolies controlling the custody, loan, and exchange of money would be irrecoverably shattered. Nation-state monopolies on the issuance and control of currency would erode.

There is a lot of parallel between Visa and Web3. Optimists would point to Visa’s current size and justify a bullish outlook on Web3. Look at its $22 billion of annual revenue at a 68% margin! The Leviathan has manifested itself!

A more cautious and nuanced view is to see Visa as a cautionary tale. How can we tame this Leviathan such that it does not eat away merchants’ profit via interchange fee. Visa’s system is broken to begin with. It has to continuously re-route value from merchants into the issuing bank. This ensures more and more banks signup to Visa, further consolidating its network effect. This mechanism might persist on Web3. However, instead of re-routing value to the wealthy class of shareholders of Visa, value is re-routed to the commons, the token-holders. Yet, even with the redistribution of value, power imbalance persists. For example, Web3 is especially over-financialized. To build a distinct and responsible Web3 might require stronger ideological and cultural forces that outweigh the expansion of cryptoeconoimcs logic.

Just as Brunton pointed out that electronic money can be a control apparatus for the government to strangle and induce its citizens, he made another delightful reference: Gilles Deleuze’s Postscript on the Societies of Control. Foucault’s disciplinary societies consist of confining enclosures. Family, school, barracks, factory, the prison, and hospital. For example, the assembly line and the factory represented efforts to enclose the labor of groups of individuals and harness their labor for productive ends. Towards the end of the twentieth century, however, Deleuze saw the emergence of a control society. It is a new form of violence and manipulations of power, coupled with capitalism’s new method of profit-seeking.

Money differentiates between the two societies. Disciplinary societies are ‘related to molded currencies containing gold as a numerical standard,’ control societies can be ‘based on floating exchange rates, modulations depending on a code setting sample percentages for various currencies.’ Today, art lies on a circuit of banking, businesses have souls, and the new ’confinement’ is ‘debt.’

Control is short-term and rapidly shifting, but at the same time continuous and unbounded, whereas discipline was long-term, infinite, and discontinuous.

A man is no longer a man confined but a man in debt.

It is a pity that Deleuze could not live long enough to see the invention of Central Bank Digital Currencies (CBDC). Imagine 'programmable money' that restricts how, when and where your citizens spend that money. Sit tight in your palace. Click a button on the screen. Vóila! You have conducted surgical monetary policy. Now the inflation rate is whatever what you want.

Control breaks an individual into ‘dividual’ — composable factors.

...imagine a city where one would be able to leave one’s apartment, one’s street, one’s neighborhood, thanks to one’s (dividual) electronic card that raises a given barrier

In addition, technology underpins societies of control. Disciplinary societies employ primary forms of technology e.g. levers, pulleys and steam engines. Control societies employ digital technology. This is a Deleuzian mutation of capitalism, where capitalism is ‘no longer involved in production, which it often relegates to the Third World…’ Instead, it becomes:

What it wants to sell is services and what it wants to buy is stocks. This is no longer capitalism for production but for the product, which is to say, for being sold or marketed. Thus it is essentially dispersive, and the factory has given way to the corporation.

The British Empire faded away its territorial control over the globe. Instead, it climbed higher and became the Financial Empire. The United States ceased its territorial expansion in North America. Instead, it turned the crown jewel of New Netherland into the global centre of Debt.

Web3 is not immune from control societies. The dominant narrative of Web3 is emancipatory: break free from Big Tech, bring our data, own our value. What difference does it make when we subjugate ourselves to the virtual movement of bits and the market-making power of profit-seeking institutions founded by elites? Axie Infinity, a play-to-earn game with millions of players from emerging markets, claims itself to be an emerging market of itself, on the metaverse. Web3 is the 21st-century control society. This is no longer a capitalism for production nor product, but bits. The corporation has given way to the metaverse.

One of the most important questions will concern the ineptitude of the unions: tied to the whole of their history of struggle against the disciplines or within the spaces of enclosure, will they be able to adapt themselves or will they give way to new forms of resistance against the societies of control?

The Ouroboros of Web3 promised to be emancipatory. That promise becomes illusionary.

The coils of a serpent are even more complex than the burrows of a molehill.

The diffusion of power locks us under the cages of capitalism. We need new weapons.

The Ontology of Money

The other main thread in the book questions the ontology of money — what are the properties that constitute the being of money? Intuitively, we would think that money is valuable. For Brunton, to examine this intuition is to face an epistemic challenge: how do we know if a currency is valuable? To some, value entails physical scarcity. To others, value simply implies cultural acceptance. To Finney, founder of B-money, a precursor to Bitcoin, money is fundamentally about bits. To Bitcoin maximalists, value equates to the transfer of energy from atoms to bits.

Yet, value is only one of the many properties of money. As a medium of exchange, money also posesses instrumental properties. Money needs to be ‘available but scarce’, ‘unique and anonymous but identifiable and reliable’, and ‘easy to transmit but impossible to copy’. These ‘paradoxical and impossible demands’ underpins the difficulty of creating digital cash.

For Brunton, however, bitcoin is disappointingly not an ontological experiment about what makes money valuable. He expected Bitcoin to contribute to an ontological debate similar to the one between Keynes and White at Bretton Woods post-WWII. Keynes presented a type of global settlement money based on agreements and utility of trade. White argued for a gold exchange standard with the US dollar as the world’s reserve currency. Until 1971, White won.

Rather, Bitcoin is evaluative, not ontological. Users have to ‘trust in yourself’ to verify records of creation, ownership and transaction in the blockchain ledger. There are no bitcoins, only the rights to trade within the closed ledger. Rather than a transactional currency, as he asked, ‘why would you spend or invest a currency that might increase in value?’. Bitcoin is insufficiently digital cash. Bitcoin (and as he extrapolates, its succeeding cryptocurrencies) is a wasteful effort to build ‘the most abstract fantasies of value ever conceived’. Here is a hint at his dissatisfaction at technological solutionism:

It may well be the purest and most honest expression of a society that could not figure out what to do with its technological inventiveness—its energy, innovation, and abundance—except to squander it in creating new kinds of artificial scarcity: the monumental folly of our age.

Yet still, what makes Bitcoin valuable? Brunton did not pick his side. Bitcoin may look like either a realistic alternative asset to a fiat-based financial system. A system where the sovereign plays inflation to its advantage, cheating economic growth boost while offloading debt. Equally likely, Bitcoin is simply a pyramid scheme where the late adopters pay for the early adopters.

Money is only necessary because of scarcity. Money measures a good’s perceived and physical scarcity in relation to other goods’. Further, scarcity is simply a lack of sufficient supply of energy (in Joules) to meet the demands of civilization. Hence, energy certificates pioneered by the Technocracy movement seem to be a reasonable reduction of money and a closer proxy of scarcity. This variance in cost per unit of energy generated has persisted since Industrialization. It renders energy non-fungible. In addition, energy loss via transmission also renders energy un-tradable. Allow me to indulge in this thought experiment: in a Green Revolution future where nuclear energy massively pushes cost curves down and large-scale off-grid energy storage becomes popular, would it be at least easier to trade energy than to trade gold? To push this eve n further, would energy units be a good candidate for inter-planetary, or even inter-galactic, trade?

Ending notes

As seen above in my discussion about energy certificates, the book does wonder in pointing readers at interesting lines of further investigation. In a podcast interview, Brunton explained that Digital Cash comes about because the subjects in his previous book, Spam, are early power users of cryptocurrencies. I wonder what Brunton will write about as the intellectual successor to Digital Cash.